Research on location theory taking into account the registered address of enterprises

Received date: 2021-04-15

Accepted date: 2021-08-22

Online published: 2022-04-10

Copyright

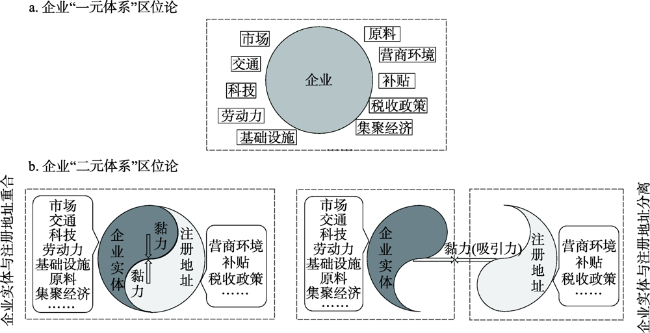

The research of location theory has long ignored the registered address as the basic attribute of the enterprise and confused it with the enterprise entity. This paper reviews the limited research in geography, economics, management, and law to elaborate on the registered address as the new location subject, the phenomenon of separation between enterprise entities and registered addresses, and the new logic of locational analysis in the context of this phenomenon, in order to extend the location theory. The main conclusions include: (1) The registered address, which is virtual and unique in nature, determines the territorial jurisdictional affiliation of matters such as supervision, penalties, and judicial enforcement to which the enterprise is subject. The location of the registered address is mainly influenced by institutional-level factors such as taxes, subsidies and administrative environment. Enterprises registered in different regions face different development prospects, while the establishment and cancellation, incoming and outgoing of a enterprise's registered address affects the region's financial revenue, regional image, and officials' performance evaluation. (2) The separation between enterprise entity and registered address has been more common. The registered address of such enterprises is located in economic zones such as free trade zones and development zones with policy advantages, and the proportion of underdeveloped areas is higher than that of enterprise entities, which are usually located in economically developed areas. Although the separation between enterprise entities and registered addresses allows enterprises to combine location and policy advantages and promote market dynamics, it has extensive negative impacts on regional development, governmental supervision and the enterprises themselves. (3) The introduction of registered address will revolutionize the traditional location theory. In the context that enterprise entity and registered address are not always the same, the traditional one single location system of “enterprise” should be adjusted to dual location system of “enterprise entity-registered address”. In the dual location system, the “stickiness” between enterprise entity and registered address makes it necessary for future location theory research not only to identify whether the location subject is an enterprise entity or a registered address, but also to distinguish the location relationship (overlap or separation) between the two when analyzing location impact, location factor, location migration, etc., and to be aware of the interaction between enterprise entities and registered addresses under different location relationships.

Key words: location theory; business entity; registered address; enterprise geography; China

HU Guojian , LU Yuqi , HU Shuyun . Research on location theory taking into account the registered address of enterprises[J]. GEOGRAPHICAL RESEARCH, 2022 , 41(2) : 580 -595 . DOI: 10.11821/dlyj020210330

表1 中文文献中企业实体与注册地址分离的案例Tab. 1 Some cases of separation of business entity and registered address in academic research |

| 作者 | 论文题名 | 具体内容 |

|---|---|---|

| 毕秀晶,等 | 《上海大都市区软件产业空间集聚与郊区化》[43] | “企业迁移路径具有明显的郊区指向性。发生区际迁移的企业规模各异,大中小企业都有,但多是注册地址与办公地址不相同的企业,例如……” |

| 沈建华,等 | 《进口非特殊用途化妆品境内责任人事中事后监管方式刍论》[44] | “(上海市进口非特殊化妆品企业)实际办公地址与注册地址不一致的情况较普遍,占企业总数的76%” |

| 张莉莉 | 《H招商管理公司的企业公众合作策略研究》[45]30 | “在H公司(上海市徐汇区的某招商管理公司)辖区内,实地注册企业占比较少,虚拟注册企业3368家,占比75.55%” |

| 韩荣 | 《仲裁送达对民事诉讼送达的借鉴作用分析》[46] | “深圳前海自由贸易区的优惠政策吸引了不少外地公司企业前来注册,但其实际办公地址仍在深圳以外区域” |

| 夏丽杰 | 《商事制度改革背景下市场主体信用监管问题研究:以T区为例》[47]21 | “2015年,山东省工商局在T区随机抽査264户企业,有29家通过登记住所无法联系,占抽查企业总数的10.98%。2016年,山东省工商局在T区随机抽查346户企业,有32户企业通过登记的住所无法联系,占抽査企业总数的9.25%” |

| 李德洗,等 | 《商事制度改革效应 研究》[48] | “基于河南6400个企业的调查结果显示,因注册地址不准确和联系方式有误而联系不上的企业占32.05%,甚至有很多企业,其注册地址是酒店房间、早已拆迁的荒地、孤寡老人居所” |

| 丁媛媛 | 《雄安新区县域电子商发展特征及区域效应》[49]39 | “1091个网络店铺样本中,发现有73家网络店铺的店铺注册地址与实际所在地址不一致,这73家网络店铺的注册地址均在雄安新区三县县范围内,但店铺实际所在地分布在保定市、北京市、衡水市、义乌市、常州市、广州市” |

| 张蓓蓓 | 《上海市外商投资企业登记制度改革研究》[50]31 | “外商投资企业注册地址与实际经营地址相分离的情况越来越严重,在经济小区的注册地址内一般无人办公,只是为了落户需要,由经济小区提供办公地址进行登记” |

| 吉昌明 | 《关于借壳上市的实证研究:基于中国市场的实证分析》[51]44 | “在借壳成功的案例中,多数企业的经昔或办公地址与注册地址不相同,注册地址一般仍为之前壳公司的注册所在省市,而经营或办公地址是借壳方的实际运营地址” |

| [1] |

冯邦彦, 叶光毓. 从区位理论演变看区域经济理论的逻辑体系构建. 经济问题探索, 2007, (4):90-93.

[

|

| [2] |

管驰明, 姚士谋, 陆树建, 等. 基于全球区位论的城市发展研究: 以江苏省南通市为例. 人文地理, 2003, 18(4):69-74.

[

|

| [3] |

贺灿飞, 刘洋. 产业地理集中研究进展. 地理科学进展, 2006, 25(2):59-69.

[

|

| [4] |

李小建, 李国平, 曾刚, 等. 经济地理学(第三版). 北京: 高等教育出版社, 2018: 19.

[

|

| [5] |

胡国建, 金星星, 陆玉麒, 等. 中国上市公司总部与注册地跨城市分离的格局、形成过程和影响因素. 地理研究, 2021, 40(2):402-418.

[

|

| [6] |

张琳. 商事登记制度改革研究: 以上海长宁区实践为例. 上海: 中共上海市委党校, 2018: 6.

[

|

| [7] |

杜恂诚. 1928—1937年中国的新设企业与政府投资. 中国社会科学, 2015, (3):158-179, 209.

[

|

| [8] |

刘孟阳, 林爱文. 基于空间分析方法的武汉市创意产业空间集聚演化研究. 人文地理, 2015, 30(6):113-120.

[

|

| [9] |

张志斌, 公维民, 张怀林, 等. 兰州市生产性服务业的空间集聚及其影响因素. 经济地理, 2019, 39(9):112-121.

[

|

| [10] |

吕铁, 王海成. 放松银行准入管制与企业创新: 来自股份制商业银行在县域设立分支机构的准自然试验. 经济学(季刊), 2019, 18(4):1443-1464.

[

|

| [11] |

郭小年, 邵宜航. 行政审批制度改革与企业生产率分布演变. 财贸经济, 2019, 40(10):142-160.

[

|

| [12] |

|

| [13] |

|

| [14] |

|

| [15] |

郭富青. 我国企业住所与经营场所分离与分制改革的法律探析. 现代法学, 2020, 42(2):145-156.

[

|

| [16] |

汪雨卉. 多源大数据视角下上海市初创企业集聚演化特征研究. 上海: 上海师范大学, 2019.

[

|

| [17] |

郭富青. 我国企业住所制度及改革的法理检讨与前瞻性构想. 上海政法学院学报: 法治论丛, 2020, (2):87-104.

[

|

| [18] |

|

| [19] |

|

| [20] |

|

| [21] |

|

| [22] |

|

| [23] |

|

| [24] |

|

| [25] |

步丹璐, 刘静. 政策性负担与民营企业行为: 基于三一重工变更注册地的案例研究. 财经研究, 2017, 43(5):65-75.

[

|

| [26] |

朱超. 自贸区背景下宁波FT贸易公司发展战略研究. 杭州: 浙江理工大学, 2017.

[

|

| [27] |

|

| [28] |

|

| [29] |

|

| [30] |

|

| [31] |

|

| [32] |

杨梦露. 经济开发区影视产业税收政策研究: 以霍尔果斯经济开发区为例. 商业会计, 2019, (21):125-129.

[

|

| [33] |

潘峰华, 夏亚博, 刘作丽. 区域视角下中国上市企业总部的迁址研究. 地理学报, 2013, 68(4):449-463.

[

|

| [34] |

何柳明. 注册地变更与政府补助: 来自中国上市公司的经验证据. 成都: 西南财经大学, 2016.

[

|

| [35] |

|

| [36] |

全怡, 严丽娜, 刘磊. 注册地变更与企业费用粘性: 基于政策性优惠和负担的视角. 会计研究, 2019, (8):47-54.

[

|

| [37] |

|

| [38] |

潘杰. 我国公司登记公示制度的缺陷与完善. 天津: 天津师范大学, 2014: 10-11.

[

|

| [39] |

王艳丽, 钟奥. 地方政府竞争、环境规制与高耗能产业转移: 基于“逐底竞争”和“污染避难所”假说的联合检验. 山西财经大学学报, 2016, 38(8):46-54.

[

|

| [40] |

张旭, 余方正, 徐良佳. 基于文化产业企业网络视角的中国城市网络空间结构研究. 地理科学进展, 2020, 39(1):78-90.

[

|

| [41] |

|

| [42] |

孙丽萍. 企业注册地变更的政府补助研究. 全国流通经济, 2019, (23):103-105.

[

|

| [43] |

毕秀晶, 汪明峰, 李健, 等. 上海大都市区软件产业空间集聚与郊区化. 地理学报, 2011, 66(12):1682-1694.

[

|

| [44] |

沈建华, 王志闻, 吴洁, 等. 进口非特殊用途化妆品境内责任人事中事后监管方式刍论. 中国市场监管研究, 2019, (2):62-65.

[

|

| [45] |

张莉莉. H招商管理公司的企业公众合作策略研究. 上海: 上海外国语大学, 2017.

[

|

| [46] |

韩荣. 仲裁送达对民事诉讼送达的借鉴作用分析. 法制与社会, 2020, (5):100-102, 115.

[

|

| [47] |

夏丽杰. 商事制度改革背景下市场主体信用监管问题研究: 以T区为例. 泰安: 山东农业大学, 2017.

[

|

| [48] |

李德洗, 张晓波. 商事制度改革效应研究. 中国市场监管研究, 2017, (11):11-15.

[

|

| [49] |

丁媛媛. 雄安新区县域电子商发展特征及区域效应. 石家庄: 河北师范大学, 2020: 39.

[

|

| [50] |

张蓓蓓. 上海市外商投资企业登记制度改革研究. 上海: 上海交通大学, 2011.

[

|

| [51] |

吉昌明. 关于借壳上市的实证研究: 基于中国市场的实证分析. 上海: 复旦大学, 2014: 44.

[

|

| [52] |

|

| [53] |

|

| [54] |

魏星. 在沪跨国公司地区总部现状及其经济效应分析. 上海: 复旦大学, 2008: 55.

[

|

| [55] |

马锦怡. 京津冀一体化对区域经济发展的影响研究. 北京: 北京林业大学, 2020: 15.

[

|

| [56] |

叶果, 李欣. 上海建筑设计创意产业空间演变研究. 见:中国城市规划年会. 城乡治理与规划改革: 2014中国城市规划年会论文集, 2014: 525-537.

[

|

| [57] |

贾宸. 企业并购动因、方式及后果研究: 基于友谊股份合并百联股份案例. 苏州: 苏州大学, 2015: 14.

[

|

| [58] |

刘清, 姚晟. 从异地经营探讨对企业住所的管理. 工商行政管理, 2005, (20):21-23.

[

|

| [59] |

李广隆. 科学防控公司登记注册地址风险探究. 中国市场监管研究, 2018, (2):72-74.

[

|

| [60] |

朱韬. 政府竞争理论视角下基层政府招商引资无序竞争问题研究: 以杭州市K街道为例. 杭州: 浙江工业大学, 2018.

[

|

| [61] |

毕梵森. 昆明市跨区域税务稽查局部门协作研究. 昆明: 云南财经大学, 2020: 21.

[

|

| [62] |

李博琦. 汇丰银行广州分行客户金融犯罪风险评级体系优化研究. 兰州: 兰州大学, 2019: 38.

[

|

| [63] |

李承蔚. 注册地址与实际地址不符, 能判定中标无效吗?. 中国招标, 2018, (45):37-39.

[

|

| [64] |

郭婧婷, 陶书宁. 霍尔果斯“转折”. 商讯, 2018, (12):5-8.

[

|

| [65] |

蒋大兴. 徒增的商事成本: 法律及管制如何影响企业设立(行为)?. 法学家, 2016, (1):72-83, 177.

[

|

| [66] |

朱华友, 朱之熹, 张林. 集聚的原生性特征与地区转型发展的理论分析框架. 经济地理, 2018, 38(10):111-117, 126.

[

|

| [67] |

刘行, 赵晓阳. 最低工资标准的上涨是否会加剧企业避税?. 经济研究, 2019, (10):121-135.

[

|

| [68] |

张敏, 刘耀淞, 王欣, 等. 企业与税务局为邻: 便利避税还是便利征税?. 管理世界, 2018, 34(5):150-164.

[

|

| [69] |

|

| [70] |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}