1 引言

20世纪50年代以来,随着通讯技术进步及交通运输业的发展,产业空间组织模式不断发生变化,模块化生产与离岸外包给交钥匙供应商的生产特征越发明显,从而在全球范围内形成新国际劳动分工[5⇓-7]。尤其以电子信息制造业最为典型,产业组织开始实现从早期的垂直一体化生产模式向水平分工的模块化生产模式和离岸外包转变,进而推动整个零部件生产体系的全球分工[8]。早在20世纪60年代,以美国电子企业为先驱,离岸生产及跨国垂直一体化就已经开始出现,如美国最早将集成电路中的封装测试环节转移到中国香港、马来西亚等地[9⇓-11]。到20世纪80、90年代以后,全球生产组织的碎片化和空间分散化过程更加明显,且这一过程与经济全球化紧密相连,生产的跨国或跨地区分工和转移趋势更加显著[12]。很多国家都被纳入到同一产品生产体系,逐步构筑起基于全球价值链的生产组织体系[10,13⇓⇓-16]。随着电子信息制造业的地理扩张,东亚地区逐渐成为承接全球电子信息制造业转移的核心地区[6,17]。尤其是以中国为代表的新兴经济体,进一步承接发达国家的外商投资及生产转移,逐步发展为全球电子制造业重要生产基地和终端市场目的地[6,15,18⇓-20]。就全球尺度来看,电子信息制造业全球价值链呈现较强的多元化特征,标准、品牌及研发等高端环节主要布局在美国、欧洲及日本等发达国家,同时日本、韩国及中国台湾在附加值较高的关键零部件生产上具有较强的技术垄断性,马来西亚、泰国和菲律宾等东南亚国家也在价值链中、高端环节零部件生产上因承接欧美产业转移而具有一定优势,而一般零部件和组装加工环节主要布局在以中国、越南和印度等具有劳动力成本比较优势的发展中国家[21⇓⇓-24]。由于各个国家或地区在电子信息制造业全球价值链中的地位不同,导致其获得的价值分配收益存在较大差异。例如,Dedrick等发现在苹果Video iPod中,苹果公司获取了其产品价值收益的36%,美国供应商获得了3%,日本供应商获得了12%,韩国供应商获得0.4%[25]。同样,还有研究发现,2010年前的苹果产品中,中国仅获得其价值分配收益的1.8%~2%[26]。然而,随着中国创新技术水平的逐步提升,多篇研究发现中国呈现出向苹果产品零部件全球价值链中、高端环节攀升趋势,但此类研究仍相对较少[6,23,24]。就驱动机制来看,研究发现贸易自由化、信息通信技术进步以及市场竞争三大要素起主要作用[27]。更进一步,Yeung从终端市场需求反映和中间市场客户关系两个层面讨论市场需求对芯片产业转移到东亚地区作用机制[28]。

总结而言,现有研究主要存在以下几点值得深入的地方:第一,尽管现有研究关注到不同国家在全球价值链中的总体地位存在差异,但国家层面的全球价值链分布特征以及各国和各地区在其中的地位变化研究仍相对较少[6,22,24]。第二,关于不同价值链环节在微观城市尺度的分布变化研究较少[29,30]。尤其像苹果公司,其零部件主要通过外包给其全球不同国家供应商来生产完成,从全球价值链视角分析这些供应商的城市区位选择与变化,对于揭示全球电子信息制造业微观布局与新近变化具有重要指示意义。第三,关于驱动机制,尽管已有研究尝试从技术进步、贸易自由化以及市场需求等因素进行分析[27,28],同时考虑地方比较优势如劳动力、土地等成本要素或区位条件的影响,但对技术管制在其中的作用关注相对不足。尤其当前受美国在高技术领域对华“脱钩”、新冠肺炎疫情以及逆全球化影响,以美国为首的发达国家试图通过“近岸外包”和“友岸外包”来重建全球产业链、供应链和价值链,并通过限制技术出口和科技打压来遏制中国产业技术升级,但经济地理领域对此展开的研究较少。

基于上述分析,本文主要贡献在于:首先,刻画了苹果品牌和研发、高、中、低价值以及组装代工等不同零部件环节的利润率差异,对电子信息制造业的价值链“微笑”曲线作了更加深入细致分析,并分析各国国家或地区在其中的总体地位。第二,从宏观国家层面和微观城市层面深入揭示了苹果产品零部件全球价值链的基本格局与变化趋势。第三,尝试从全球化、市场化、地方化以及技术管制四个方面,用全球与地方、市场与管制相互对应的思路揭示苹果产品零部件全球价值链的形成机制,为消费电子全球价值链的形成提供一种新的解释视角。

2 数据来源与研究方法

2.1 数据来源

数据源于苹果公司官网(

2.2 苹果产品零部件价值链分级

关于苹果产品零部件的价值划分,主要参考iSuppli Corp.、Portelligent Inc.、野村证券(加特纳)公司、《2012智能手机指南》等报告关于苹果产品零部件的物料成本拆解报告以及多位学者关于电子或苹果产品零部件价值分级研究成果的基础上[6,10,11,16,23⇓-25,31⇓-33],按照零部件成本价值及技术含量大体划分为高、中、低价值零部件三类,见表1。具体而言,高价值零部件环节主要指技术含量高、可替代性弱且成本较高的零部件,如芯片设计代工和制造代工、面板模块、相机模块等,如三星、高通、台积电、索尼等企业;中等价值零部件环节主要指技术含量相对较高、替代性较强且价值含量一般的零部件,如声学器件、连接器、印刷电路板(FPC、PCB)等;低价值零部件技术含量很低、替代性很强且价值含量较低的零部件,如芯片封装测试、键盘、铰链和枢轴、外壳、包装印刷以及组装代工等。需要说明的是,尽管芯片封装测试是芯片中重要一环,但鉴于其工艺成熟、技术门槛较低且属于劳动密集型行业,故将其列为低价值零部件环节。

表1 基于成本价值的苹果产品零部件等级标准

Tab.1

| 价值链分级 | 零部件名称 |

|---|---|

| 高价值零部件环节 | 芯片设计代工和制造代工(3D指纹传感器芯片、基带芯片、内存芯片、闪存芯片、射频芯片、电源管理芯片、触控芯片、分立器件、模拟信号芯片、无线通信芯片等)、面板模块(LED驱动芯片、背光模组、彩色滤光片、液晶面板、玻璃基板)、相机模块(镜头、模组、图像传感器等) |

| 中等价值零部件环节 | FPC、PCB、电池、充电器、数据线、MLCC电阻、电容、电感、振动器、精密马达、 连接器、散热组件、晶振、耳机、扬声器、精密组件、聚碳酸酯、硬盘等 |

| 低价值零部件环节 | 芯片封装测试、金属与塑料外壳、键盘、结构件、塑胶材料及辅料、铰链和枢轴、模具、功能材料、金属材料、包装印刷品和整机组装代工等 |

2.3 赫芬达尔指数

赫芬达尔指数是用来测度集中分布程度的重要指标。本文利用该指标来反映不同价值链环节供应商子公司分布的国家或地区集中程度,计算方法如下:

式中:

2.4 区位熵

区位熵是反映某一产业部门是否在整个产业体系中具有比较优势的指标。本文借鉴区位熵反映比较优势的思想,用该指标测度不同国家或地区在苹果产品零部件全球价值链中供应商子公司数量分布上是否具有比较优势,计算方法如下:

式中:

3 苹果产品零部件全球价值链总体特征与分布格局变化

3.1 苹果产品零部件价值链“微笑”曲线与供应商总体变化特征

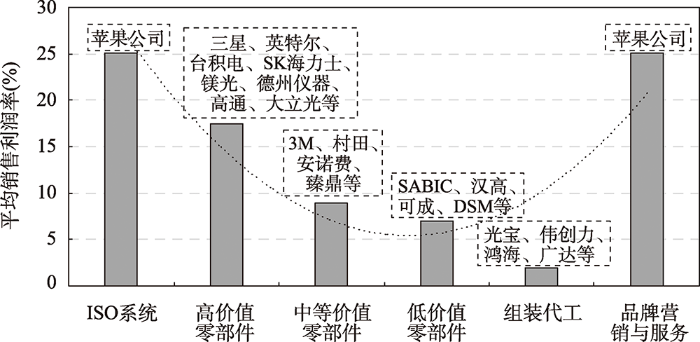

首先,选择2020年苹果供应商中的上市公司,通过逐一搜索发现有156家上市公司,剔除2018—2020年这三年平均销售利润为负的企业,得到147家样本。计算2018—2020年不同价值链环节供应商及苹果公司的年平均销售利润率,刻画了苹果产品零部件价值链“微笑”曲线。正如图1所示,发现各个环节销售利润率差距非常明显。其中,苹果公司控制了价值链曲线的两端(系统和品牌),且平均销售利润率高达25.1%;其次是高价值零部件供应商,平均销售利润率为17.5%,主要以三星、英特尔、台积电、高通等芯片及面板企业为代表,主要来自美国、韩国和中国台湾;中国生产闪存芯片的兆益创新和玻璃盖板的蓝思科技两家企业的销售利润率较高,而京东方和欧菲光这两大重点企业的盈利能力较低;中等价值零部件供应商的销售利润率次之,平均销售利润率8.9%,主要企业有3M、村田、安诺费、歌尔声学、瑞声科技等,来自日本、中国、中国台湾以及美国;低价值零部件供应商的平均销售利润率约为7.0%,如SABIC、汉高、可成、DSM、精研科技、江苏长电等企业,主要来自中国和中国台湾;组装代工环节供应商的平均销售利润率最低为1.9%,主要以光宝、伟创力、鸿海、广达、和硕等企业为主。

图1

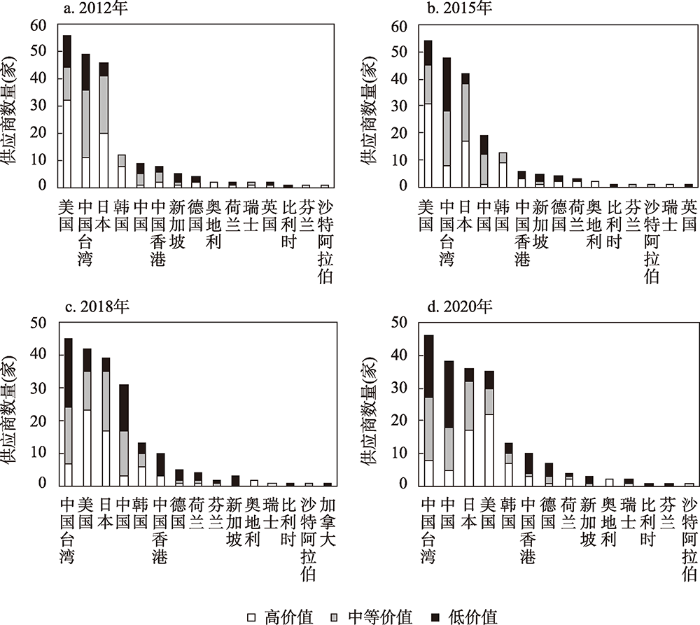

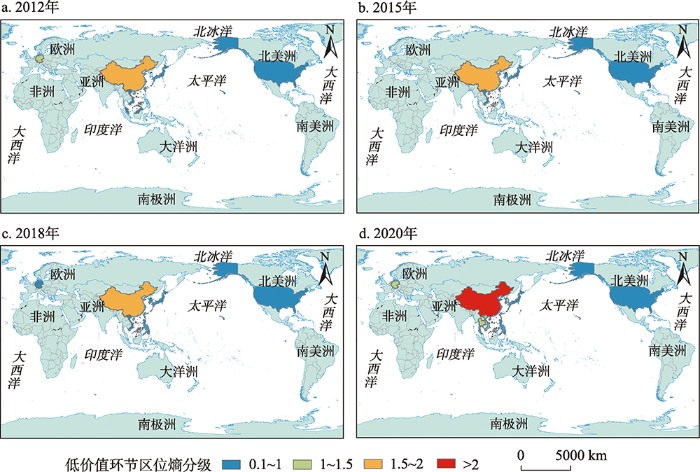

其次,图2展示不同国家供应商在苹果产品零部件全球价值链中总体地位,可知2012—2020年苹果产品零部件供应商由“美国、中国台湾、日本”三足鼎立,转变为“中国、中国台湾、美国、日本”四强格局,中国地位抬升明显。美国供应商数量呈明显缩减趋势,日本和中国台湾也呈现波动下降趋势,而中国供应商数量则增加明显。具体看来,高价值零部件环节由美国为主导,日本、中国台湾、韩国为多强的“一超、多强”转变为美国、日本为主导,中国、中国台湾、韩国为多强的“双核、多强”格局。美、日控制价值链的高端环节,中国在价值链高端环节有所攀升;中等价值零部件环节以中国台湾、日本、美国为核心,中国、韩国、中国香港为外围的“多核-外围”格局演变为中国台湾为主导,日本、中国两强,美国、韩国、德国等为外围的“一超、两强、外围”格局。低价值零部件环节由“美国、中国台湾为主导,日本、中国、新加坡等为外围”转变为“中国、中国台湾为主导,中国香港、美国、德国等为外围”的“双核-外围”空间特征,中国代替美国成为低价值零部件核心供应国。

图2

图2

2012—2020年低、中、高价值零部件供应商分布

Fig. 2

Distribution of suppliers in different value chains from 2012 to 2020

3.2 苹果产品零部件全球价值链宏观格局变化

基于2012—2020年各个国家或地区布局的供应商子公司数量,分别从总数及高、中、低三个环节计算前四、三、二、一大国家的赫芬达尔指数和占比情况①(①之所以选择前四、三、二、一大国家进行计算,主要因为供应商子公司具有非常强的少数国家集中分布特征。就供应商子公司整体分布而言,集中在中国、日本、美国、韩国等四个国家;具体到价值链的不同环节而言,高价值零部件环节集中分布在中国、日本和美国,中等价值零部件环节集中分布在中国和日本,低价值零部件环节集中分布在中国,而其余国家分布数量很少,故未纳入分析。),见表2。

表2 2012—2020年苹果产品零部件全球价值链地理分布局域特征

Tab. 2

| 年份 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2020 | 分布区域 |

|---|---|---|---|---|---|---|---|---|---|

| S前四大国家HHI | 0.2182 | 0.2310 | 0.2381 | 0.2384 | 0.2416 | 0.2530 | 0.2560 | 0.2555 | 中国 中国台湾 日本 美国 韩国 |

| S前四大国家数量 占比(%) | 79.05 | 78.68 | 80.29 | 79.67 | 80.51 | 82.24 | 82.80 | 81.50 | |

| H前三大国家HHI | 0.1209 | 0.1273 | 0.1233 | 0.1227 | 0.1200 | 0.1288 | 0.1304 | 0.1257 | 中国 日本 美国 |

| H前三大国家数量 占比(%) | 59.41 | 60.28 | 60.25 | 59.94 | 59.52 | 60.14 | 61.48 | 59.60 | |

| M前二大国家HHI | 0.2796 | 0.2642 | 0.2729 | 0.2580 | 0.2716 | 0.2723 | 0.2846 | 0.2785 | 中国 日本 |

| M前二大国家数量 占比(%) | 71.43 | 67.14 | 69.14 | 67.77 | 69.23 | 69.11 | 70.94 | 70.80 | |

| L第一大国家HHI | 0.5378 | 0.6060 | 0.6400 | 0.6173 | 0.6167 | 0.4877 | 0.5008 | 0.5006 | 中国 |

| L第一大国家数量占比(%) | 73.33 | 77.84 | 80.00 | 78.57 | 78.53 | 69.83 | 70.77 | 70.75 |

注:S为供应商子公司总数;H为高价值零部件环节;M为价值零部件环节;L为低价值零部件环节。

尽管赫芬达尔指数均存在波动,但证实具有非常强的少数国家或地区集中分布特征。其中,低价值零部件环节的集中度最高,赫芬达尔指数总体呈先上升后下降趋势,表明第一大国家仍具有集中分布优势;从占比情况看,低价值零部件环节集中布局在中国,虽总体呈先增后降特征,表明尽管低价值零部件环节倾向于布局在中国,但是其他国家或地区出现一定的分流趋势;中等价值零部件环节的赫芬达尔指数次之,虽有所波动但变化较小,集中布局在中国和日本,二者合占该环节全球分布总数的2/3;供应商子公司总体分布也呈现出较强的局域集中特征,且呈现出波动增加趋势,说明总体向中国、日本和美国等四个国家集中;更进一步,前四大国家的供应商子公司数量占了全部数量的80%以上。最后,高价值零部件环节的局域集中度最低,总体呈现较为稳定趋势,说明其在全球分布相对稳定,且集中向中国、日本和美国进行布局,占比接近60%。

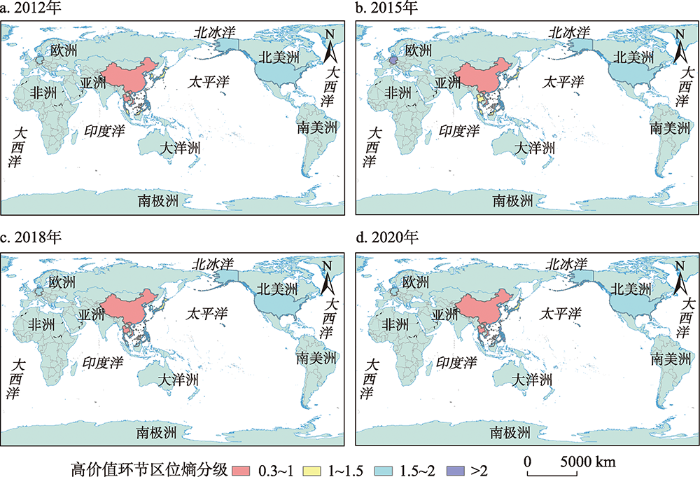

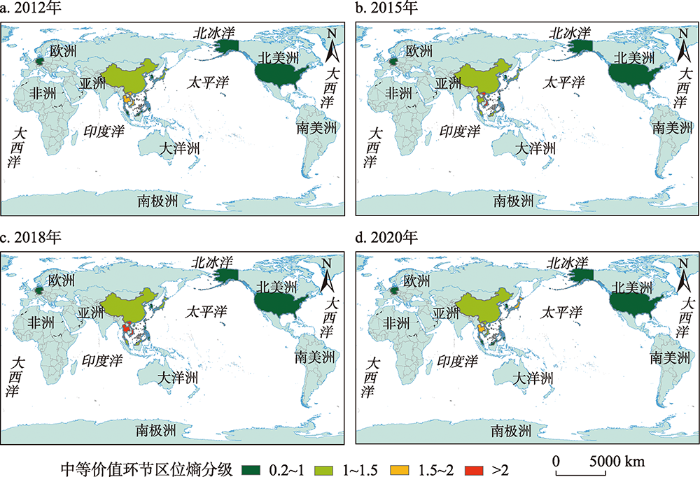

更进一步,利用区位熵方法计算各个国家或地区在高、中、低价值零部件环节的分布数量比较优势,并选取供应商子公司总数占比前十的国家或地区进行分析②(②2012—2020年排在前十中的国家或地区基本没变,仅德国被越南代替,因此四个节点年份中将两国都纳入分析。),结果见图3、图4、图5(见第624页)。发现美国、德国、日本、韩国、中国台湾以及少数东南亚国家在价值链中高端环节具有较强的数量分布比较优势,而中国则在中、低端环节具有分布比较优势。其中,在高价值零部件环节具有分布比较优势的国家或地区集中在美国、德国、日本、韩国、中国台湾及部分东南亚国家,且总体变化较小;不过,中国台湾比较优势逐渐消失,主要是因为2012—2020年高价值零部件环节在中国台湾的布局数量较为稳定,而中、低价值零部件环节在中国台湾的分布数量有所增加所致。在中等价值零部件环节具有分布数量比较优势的国家或地区主要包括泰国、日本、越南、中国、中国台湾及马来西亚等,且随时间变化较小;在低价值零部件环节,中国明显具有分布数量上的比较优势,尽管前述中国在苹果产品零部件全球价值链中占据重要地位,且高、中、低价值零部件供应商子公司均布局较多,但集中在价值链的中低端环节;同时,中国和韩国也在低价值零部件环节具有一定的数量分布比较优势。

图3

图3

2012—2020年各国家或地区在高价值环节区位熵变化

注:该图基于自然资源部地图技术审查中心标准地图(审图号:GS(2016)1666号)绘制,底图边界无修改;图中仅显示区域熵较高且供应商子公司分布数量较多的国家或地区。

Fig. 3

The changes of location quotient in high value chain of each country (region) from 2012 to 2020

图4

图4

2012—2020年各国家或地区在中等价值环节区位熵变化

注:该图基于自然资源部地图技术审查中心标准地图(审图号:GS(2016)1666号)绘制,底图边界无修改;图中仅显示区域熵较高且供应商子公司分布数量较多的国家或地区。

Fig. 4

The changes of location quotient in medium value chain of each country (region) from 2012 to 2020

图5

图5

2012—2020年各国家或地区在低价值环节区位熵变化

注:该图基于自然资源部地图技术审查中心标准地图(审图号:GS(2016)1666号)绘制,底图边界无修改;图中仅显示区域熵较高且供应商子公司分布数量较多的国家或地区。

Fig. 5

The changes of location quotient in low value chain of each country (region) from 2012 to 2020

3.3 苹果产品零部件全球价值链微观格局变化

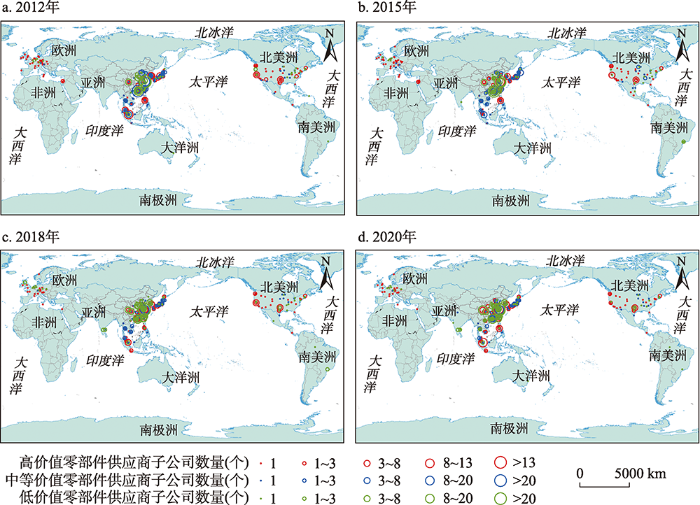

从图6可以发现,苹果产品零部件的全球生产主要集中在太平洋东、西两岸,即太平洋东岸(以美国为主)以系统研发、芯片设计等高价值零部件为主,而太平洋西岸则主要以生产各类高、中、低价值零部件为主,总体呈现出“东岸研发设计、西岸零件制造”的分布格局。更进一步,主要集中在中国、中国台湾、日本以及东南亚、南亚、西欧、北美的城市群或都市区,呈现出明显向高度城市化地区集中趋势。其中:

图6

图6

2012—2020年苹果不同价值链环节零部件供应商子公司分布变化

注:该图基于自然资源部地图技术审查中心标准地图(审图号:GS(2016)1666号)绘制,底图边界无修改。

Fig. 6

Distribution changes of supplier subsidiaries in different value chains of Apple's parts from 2012 to 2020

(1)高价值零部件环节倾向于分布在中国的长三角、珠三角、成渝以及一些地方中心城市,中国台湾的桃园-新竹-台中都市区和台南-高雄都市区,韩国首尔-龟尾市城市化地区,日本东京、大阪及名古屋三大都市圈、越南河内和胡志明都市区、泰国曼谷都市区、菲律宾马尼拉都市区、新加坡-槟城城市化地区、美国旧金山湾区、波特兰都市区、达拉斯-奥斯汀都市区以及波士华城市群周边、欧洲西北部城市化地区等。从主要变化来看,高价值零部件环节在中国的分布数量虽有所减少。但是,呈现出向武汉、赤壁、南昌、合肥等多个城市扩张趋势,主要是因为中国本土供应商向这些城市进行布局。日本东京、大版和名古屋三大都市圈呈现进一步集中趋势;在中国台湾的布局,呈现出向桃园-新竹-台中和台南-高雄两大都市区扩张趋势。在东南亚的布局,则呈现出向河内都市区和马尼拉都市区扩张趋势。西欧呈现出缩减趋势,北美相对稳定。

(2)中等价值零部件环节主要集中在中国的长三角、珠三角以及京津冀、中国台湾的台北-新竹-桃园-台南城市化地区、越南河内-岘港-胡志明城市化地区、泰国曼谷都市区、韩国首尔都市区、新加坡-马来西亚槟城地区、日本的内-外海沿线地区等多个集聚区,并呈现进一步向核心城市化地区及周边城市扩张趋势。2012—2020年进一步向中国的“苏沪锡常”和“深莞广惠”集中,并逐步向周边的扬州、淮安、嘉兴和其他如吉安、汕头、泉州、重庆等城市扩张。在日本的布局,集中在东北地方以及中部日本海沿线,但在关东地方、宫崎县等地呈退出趋势。在韩国布局较少且呈现一定退出趋势,集中于京畿道和忠清北道的安山市、始兴市、清州市等港口或新兴电子城市。在中国台湾的布局,则进一步向新竹、高雄等核心城市扩张。东南亚地区呈现进一步向河内都市区、胡志明都市区以及曼谷都市区集中。中等价值零部件环节出现向印度的北方邦Noida(近新德里)和金奈两大城市扩张趋势。北美、西欧的布局相对较少,在美国和墨西哥退出迹象明显。

(3)低价值零部件环节主要呈现向中国东南沿海大城市及周边和向內陆扩张趋势,并呈现向越南和泰国、印度、韩国以及中国台湾北部等地扩张趋势。2012—2020年构成以中国四大城市群为主导、东亚-东南亚-南亚-北美-西欧城市为外围的分布格局。更进一步,长三角、珠三角、成渝以及中原城市群的核心地位得到强化,同时向外围或一般性城市扩张。同时,少量供应商子公司逐渐向越南河内都市区、泰国曼谷都市区、印度班加罗尔-金奈等城市化地区扩张,逐步承接部分产业转移。此外,日本、韩国和中国台湾也有少量低价值环节布局,主要向韩国首尔-京畿道-庆尚北道以及中国台湾的台北-桃园-新竹等地区扩张明显,在日本的布局呈明显减少趋势。西欧、北美等也有少量布局,但总体分布较为分散。

4 驱动机制分析

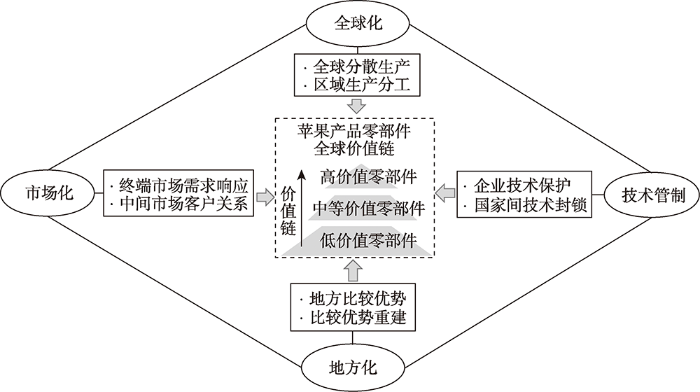

伴随科技进步与技术革新,电子产品零部件生产出现显著产品内分工趋势,推动跨国公司通过链式重构来重新组织生产活动,从而使得生产活动突破国家间的地理边界,逐渐走向生产环节的全球化布局[34]。得益于全球经济一体化的不断深入,特别是新国际劳动分工不断深化,使得跨国公司进一步在全球寻找最佳生产区位,来降低生产成本[6,35]。建立在本地要素成本、区位优势及政府的鼓励外资政策等地方比较优势的基础上,全球电子信息制造业从刚开始向亚洲四小龙扩张,随后向中国、东南亚、印度等新兴经济体扩张。同时,随着新兴经济体的快速发展,亚洲市场的重要性进一步凸显,从而吸引了电子信息制造业进一步向亚洲地区的新兴城市化地区布局,并推动了亚洲本地电子信息制造业的发展和本土企业崛起[6,17]。不过,由于企业自身的技术保护和国家间技术封锁等技术管制的影响,导致跨国公司一方面推动生产和技术之间的分离,同时由于美国增强对中国的技术封锁与高科技打压,使得跨国公司在东亚的布局不断发生变化。因此,苹果产品零部件全球价值链的形成及变化主要受全球化、市场化、地方化以及技术管制等要素综合影响(图7)。

图7

图7

苹果产品零部件全球价值链的驱动机制

Fig. 7

Influencing mechanism of global value chains of Apple's parts

4.1 全球化催生了苹果产品零部件全球价值链基本格局

经济全球化是世界经济活动跨越国界,通过国际贸易、资本流动、技术知识转移、劳动力流动等形成相互依存、相互联系的世界经济体系过程[36]。全球化与生产技术的发展进一步引发生产组织的变革,新国际劳动分工深入到产品层次,零部件生产的地区专业化分工愈发明显[37]。各国在专业化分工、规模经济等后天获得优势方面的差异,形成了以产品价值链为纽带的分布模式,即将技术核心、主要零部件以及一般性工序进行差异化布局[34,35]。在全球化背景下,苹果公司主要负责产品及系统研发设计,而将全部零部件生产和加工外包给不同的供应商,从而将全球主要国家或地区都纳入到以苹果公司为主导的全球价值链。其中,供应商中多数企业属于细分领域的全球领先跨国公司,构建了全球电子信息制造业基本格局。这些跨国公司借着经济全球化与发展中国家的经济发展政策,根据各国或地区的要素禀赋差异进行国际一体化生产布局[35]。

例如,Vishay公司在以色列Dimona市的布局中就提到受经济全球化影响很大(原话为In the mid-1980's Dimona was a struggling city. At the same time, Dr. Felix Zandman saw the force that was globalization—in this he also saw an opportunity for Israel③(③Vishay公司官网:

4.2 市场化主导了苹果产品零部件全球价值链分布格局

(1)终端市场需求响应。东亚、东南亚以及南亚地区是苹果产品的重点市场,使得苹果供应商倾向于布局在消费市场中心,这些消费市场多数是该国的核心或重点城市。接近终端市场,就近服务当地客户,能够降低市场交易成本,获得集聚经济[38]。为了占领消费市场,跨国供应商进一步向东亚、东南亚以及南亚地区的核心城市化地区或周边城市布局。除占领市场外,一些领先公司经常要求他们的主要供应商跟随他们到新的生产地点,也会影响到供应商在各个国家或地区的生产布局[3]。不过,中国以“市场换技术”的产业政策促使了供应商把技术含量较高的产品转移到中国生产[39]。例如,苹果产品零部件芯片企业Qorvo在中国北京和德州市的布局就是看重了中国巨大的市场,“全球70%的智能手机都是在中国生产,Qorvo为了保持对客户的快速响应与及时交付,在北京与德州两地建设异地统一生产体系,这也体现了Qorvo对中国市场的重视”④(④搜狐新闻:Qorvo:射频领域的半壁江山。)。再如,欧姆龙在衡阳的布局便提到“衡阳是一个非常有发展潜力的城市,手机背光板产品国际市场前景很好”⑤(⑤工控新闻:欧姆龙精密电子落户湖南衡阳。)。此外,印度市场也是苹果的重要市场,吸引了鸿海、纬创、和硕以及领益科技等组装代工跨国企业进入布局。

(2)中间市场客户关系。由于苹果产品零部件的模块化特征,使得各个零部件的生产需要通过细分零部件模块来完成,尤其是芯片、面板、摄像头等高价值链零部件[23]。就芯片而言,很多苹果产品零部件芯片企业主要属于美国芯片设计企业,只负责设计而并不生产芯片。而芯片生产企业主要靠三星和台积电完成。同时,芯片生产出来后,还要靠芯片封装和测试公司作最后调试。芯片设计企业在全球区位布局时,要靠近三星、台积电等芯片制造企业在全球的布局。同时,芯片封测企业主要来自新加坡、中国和中国台湾。这些从事芯片生产、设计以及封测的企业在全球布局时,都会考虑彼此的区位。例如,江苏长电便将封装子公司布局到了韩国三星公司附近。再如,摄像头模块就包括传感器、镜头、模组和马达等环节,这些零部件企业以日本、韩国和中国台湾的企业为主。同样,液晶屏模块、触摸屏模块以及各种电阻、声学、连接器等高、中等价值零部件供应商主要属于东亚地区的企业。因此,不同价值链环节零部件的中间产品生产商主要位于东亚地区,使东亚地区进一步成为跨国供应商布局的核心集聚区,来进一步降低中间产品交易成本。

4.3 地方化不断改变苹果产品零部件全球价值链分布格局

地方化要素着重强调本地相比于其他地区的本地比较优势或通过地方政府作用介入而创造出的新优势,主要体现为地方对经济全球化的响应。一方面,由于地方比较优势的作用,产品内分工体系下的各国家或地区结合自身区位比较优势嵌入全球价值链[40]。另一方面,地方政府也会通过政策、土地、资金等优惠政策,吸引苹果供应商子公司布局,从而进入苹果产品零部件全球价值链。因此,地方化也在不断改变着苹果产品零部件全球价值链分布格局。

(1)地方比较优势,即多重比较和竞争优势在地方上的叠加[5,41]。价值链不同环节零部件的生产对地方禀赋要求不同,不同国家或地区结合自身区位比较优势嵌入苹果产品零部件全球价值链[42]。具体看来,高、中、低价值零部件供应商子公司都倾向于向大都市区或地方中心城市布局。其中,高价值零部件供应商除将核心技术环节布局在母国之外,倾向于将国外子公司布局在西欧国家或亚太新兴工业化国家的科技中心城市,以降低交易成本[43]。核心城市占据科技和人才优势,不仅集聚了全球的资本、信息和技术,同时具有发达的市场条件、较强的科创能力[44]。中、低价值零部件环节的供应商子公司同样趋向于靠近核心城市进行布局,以降低政策风险和投入成本[38,42]。例如,和硕(代工企业)在捷克的工厂位于俄斯特拉,该市是捷克北摩拉维亚州首府且是重工业城市,同时也是重要的交通枢纽。然而,中、低价值零部件环节的供应商对成本要素较为敏感。随着通勤成本、土地租金和劳动力成本上涨,对运输成本更高、土地和劳动力需求更大的产业部门可能会向外围地区转移[45]。由于劳动力价格、资源条件等比较优势,一些全球性企业将生产地转移至发展中国家的新兴城市化地区[46]。凭借在土地、劳动力以及政策和社会环境等方面的优势成为主要承接地,形成能提供及时且成本较低生产服务的“成本节约中心”[22]。例如,富士康的苹果iPad生产放在太原,除接近劳动力所在地以外,且产品所需的镁锭原料多在山西生产,可就近在山西获得[47]。近年来,中、低价值零部件环节的供应商子公司的布局开始呈现出向越南河内都市区、胡志明都市区和印度的班加罗尔-金奈城市化地区扩张趋势,原因之一便是这两国的劳动力成本相比中国的沿海地区更低,且距海港较近,对外联系方便。同时,转移企业主要布局在核心城市周边,基础设施完善,有利于降低生产成本。

(2)地方比较优势重建。地方政策是改善区位条件的重要手段[48]。地方有为政府的招商引资手段,出台相关的税收、土地优惠政策以及各项基础设施的优先配套等也会吸引不同价值链环节供应商向该地布局[39,49]。例如,乐山市吸引了美国安森美半导体的进入布局,主要是本地拥有乐山无线电股份有限公司,政府积极推动两大公司合作,从而推动了乐山嵌入苹果产品零部件全球价值链中的高价值环节。再如,中南创发在赤壁的布局中,便提到了“维达力从签约、开工、投产,到再次追加投资,背后有一个主要原因:当地良好的投资环境”[50]。再如,郴州市为了吸引台达集团在当地布局,“将台达集团当作2007年引进的重要战略投资者,也是湖南省委、省政府重点扶持的战略产业头部企业,并提供完善的经营环境与配套措施”⑥(⑥台达新闻中心-台达将投资五千万美元扩建郴州厂区-台达(delta-china.com.cn)。)。再看越南,为吸引苹果零部件供应商布局转移,政府出台很多吸引外资的政策,尤其是税收“免二四减半”,甚至“免四九减半”,加之与欧盟签订双边自由贸易协定(EVFTA),吸引较多供应商进入布局。

4.4 技术管制深刻影响着苹果产品零部件全球价值链格局

(1)企业技术保护管制。多数高价值零部件供应商将核心技术或关键技术环节保留在母国,来保护核心技术并维持自身在关键技术环节的领先优势[3]。从苹果产品零部件全球价值链的地理分布看,供应商主要将一般生产环节转移出去,或退出这些环节,而将核心技术与高端生产环节保留在母国。尤其是硅谷地区作为芯片企业核心集聚区,主要将芯片设计核心技术环节保留在硅谷,而将价值含量较低的封装、测试环节转移到东南亚国家[9⇓-11]。另外,三星为苹果提供OLED面板和最先进的存储芯片,并未将这些核心环节布局到国外,三星在中国布局的分支企业也并非是核心环节,并且韩国高价值零部件企业呈现进一步向越南转移趋势。再如,为苹果代工芯片的台积电,虽然在中国布局了8英寸和12英寸晶圆厂,但是进入苹果供应链的所有芯片企业均位于中国台湾本土,如6英寸晶圆厂和后段封测厂都在中国台湾本土。再如,很多总部在东京的供应商将其生产布局在非东京的母国城市或东亚其他城市,仅将总部或技术核心留在东京[6]。生产MLCC(陶瓷电容器,价值含量较高)的村田制作所和太阳诱电两家日本供应商的零部件生产主要布局在日本本土,很少向母国以外国家布局。

(2)国家间技术封锁管制。近年来,随着中美关系不断变化,以美国为首的西方国家增强了对中国的高技术封锁与贸易制裁。例如,苹果供应商之一的南昌欧菲光(生产光学镜头)因被美国政府列入制裁名单,被苹果剔除供应商名单。同时,美国从多方面加强对华技术出口管制,限制本国高技术企业对华技术出口,影响到苹果供应商的在华客户市场,也会影响美国供应商在中国的布局。同时,迫于美国技术封锁政策以及保障供应链安全考虑,苹果供应商把布局在中国的一些子公司转移到其他国家或地区。尤其是,在美国科技封锁以及制造业回流政策等外部风险要素的不断影响下,会进一步影响美国供应商在中国的布局。例如,2012年美国供应商在中国的布局有64家,而到2020年仅剩49家,尤其是中、高价值零部件环节的美国供应商在中国的布局数量明显减少,如2020年芯片企业英特尔仅剩布局在大连和成都的子公司为苹果提供零部件,而布局在上海和深圳的子公司退出苹果供应商名单。

5 结论与讨论

5.1 结论

本文利用苹果公司2012—2020年供应商及其子公司数据,分析了苹果产品零部件全球价值链分布格局与变化,并从全球化、市场化、地方化以及技术管制四个方面分析了其形成与演变的驱动机制,主要结论如下:

(1)苹果公司在其价值链曲线中处于领导地位,高、中、低不同价值零部件环节的盈利水平逐渐降低,代工组装环节的获利能力最低。2012—2020年苹果供应商由“美国、中国台湾、日本”为主导转变为“中国、中国台湾、美国、日本”为主。高价值零部件环节以美国、日本双核为“龙头”,中等价值零部件环节以日本、中国、中国台湾三强作“龙身”,低价值环节以中国和中国台湾为“龙尾”,形成了一种新型联动式“龙型”发展格局。中国逐渐向“龙身”迈进。

(2)苹果产品零部件全球价值链分布具有非常强的少数国家或地区集中分布特征,尤其是中、低价值零部件环节趋向于布局在1~2个国家。从细分价值链来看,中国主要在中、低价值零部件环节具有数量分布比较优势,而高价值零部件环节具有数量分布比较优势的是美、日等发达国家或少数东南亚国家。这就说明,尽管中国尽管吸引了最多的供应商进入布局,但是集中体现为以价值链的中、低端环节为主。

(3)高价值零部件环节集中向东亚、东南亚等电子信息制造业发达的核心城市群区域或重点城市进行布局;河内都市区和成渝城市群在吸引高价值零部件环节扩张方面表现突出。中等价值零部件环节核心分布在长三角、珠三角及中国台湾的桃园-新竹-高雄组成的“长、珠、台大三角区域”,且呈现出进一步向这三大区域及周边城市集中的趋势。低价值零部件环节趋向于集中布局在长三角、珠三角、成渝及中原四大区域且呈现进一步集聚趋势;同时,向河内都市区、曼谷都市区、首尔都市区以及班加罗尔-金奈等城市化地区扩张,这些区域开始分流部分低价值零部件环节布局转移。

(4)苹果产品零部件全球价值链分布的形成与变化主要是全球化、市场化、地方化以及技术管制四个要素综合作用的结果。全球化推动了不同价值链环节基于地方比较优势、市场条件以及城市化水平等要素进行差异化布局。市场化要素则通过终端市场需求响应和中间市场客户关系推动苹果产品零部件全球价值链进一步向东亚、东南亚、西欧以及北美等地的主要城市化地区集中布局,尤其是东亚、东南亚的新兴城市化地区成为核心集聚区。地方化要素促使不同价值链环节供应商根据地方优势条件进行布局,同时,当地有为政府在推动本地嵌入苹果产品零部件全球价值链中发挥重要作用。技术管制主要因企业自身技术保护和国家间技术封锁导致很多高价值环节仍保留在母国,或推动高技术环节退出某些区域而进行新的区位选择。

5.2 讨论

(1)提升中国供应商在苹果产品零部件全球价值链中的竞争力。中国在苹果产品零部件全球价值链中地位攀升明显,尤其是在中、高等价值链环节嵌入程度加深。其中,中国的主要优势集中在价值链的中、低端环节,尤其是在生产电池、结构件、连接器以及声学器件等零件方面具有较强竞争力,并与中国台湾共同占据中、低端零部件供应商核心地位。然而在高价值零部件环节,仅兆益创新和蓝思科技两家企业盈利水平高,长电科技、京东方、深天马等芯片和面板企业的盈利水平还较低,说明尽管中国供应商在价值链高端有所攀升,但仍需提升其市场盈利能力。同时,与美国、日本、韩国等相比,中国在价值链高端环节的供应商数量还较少,在芯片设计和制造环节等关键技术环节明显处于劣势。可见,决定价值链分工地位的核心要素仍是科技水平。因此,中国迈向价值链中高端的主要途径也主要向先进制造业方向发展,从而推动构建现代化产业体系,实现价值链攀升。

(2)实施区域差异化发展策略。相比国外而言,长三角和珠三角地位稳固且向价值链的中高端环节逐渐攀升,并与中国台湾遥相呼应,可以通过构建“长粤港台大三角”零部件生产集聚区,强化供应链保障能力和推动区域价值链攀升。內陆的成渝、中原地区也已形成较强且相对稳固的苹果产品零部件的生产和组装集聚区,但是受交通、基础设施、劳动力成本等地区竞争优势日渐不足的影响,需要继续强化电子信息制造业集群化发展,防止产业链出现大规模转移;其余中西部地区的区位优势并不突出,要想承接电子信息一般产业的继续转移,虽具有较大的难度,可向郑州学习经验,通过改善地方禀赋、推进城市化建设以及政策突破等手段,通过吸引苹果供应商进入布局,逐步嵌入苹果产品零部件全球价值链。

(3)密切关注苹果产品零部件全球价值链的新近变化趋势。近年来,苹果供应商呈现出向越南、印度扩张趋势,这是一个十分重要的信号。一方面,受中国生产成本上升、国际形势变化以及各类风险要素的影响等推动着供应商向东南亚、南亚转移;另一方面,东南亚、南亚的成本优势和区位优势,以及与西方国家的自由贸易协定政策等,也在吸引苹果供应商转移。在这些要素作用下,苹果产品零部件全球价值链也在处于新的变化或重构中。例如,2012—2020年布局在越南的供应商分支数量增加了14家,尤其是红河三角洲的河内都市区集聚了12家供应商子公司。这主要是因为越南近年来出台的很多税收、土地优惠政策和劳动力成本优势,吸引了以三星为核心的供应商布局的结果。同时,2012年印度并没有苹果供应商进入布局,但到2020年已经有9家供应商子公司布局在印度,集中在班加罗尔-金奈城市化地区。尽管这些新兴经济体开始承接一些苹果供应商的进入布局,但主要以中低价值零部件供应商布局为主,且这些国家尚未崛起可以参与全球竞争的本土企业,说明这些国家仅仅承接了部分产业转移而没有实现本土企业真正崛起,不可能吸引苹果供应商大规模转移。但是,随着中美关系博弈以及2020年以来一直持续的新冠疫情等外部风险因素的影响,尤其是2022年4—5月份的上海(连锁反映影响整个长三角)封城和10月份的郑州疫情封控,对苹果供应链的稳定产生严重影响。更进一步,地方供应链中断,将会对整个产品生产与供应体系产生严重影响[51]。供应商会重新审视地理区位因素并结合风险防控考虑,导致苹果产品零部件全球价值链地理分布面临更多的不稳定性和变化[52]。因此,需要主动适应新变化,积极构建与东南亚、南亚国家的新型区域分工和合作关系。

最后,相比已有研究而言,本文印证了多位学者关于电子信息制造业价值链曲线的研究[6,22,51],同样发现产品研发和品牌占据价值链的高端,芯片、面板等关键零部件处于次一级,组装代工环节处于价值链曲线的低端,但本文不仅利用销售利润率数据精准刻画了苹果产品零部件价值链曲线,更是深入揭示了品牌和研发、高、中、低以及组装代工等不同价值链环节的利润率差异,对电子信息制造业价值链“微笑”曲线作了更加深入细致的分析。同时,本文不仅揭示了苹果产品零部件全球价值链分布的基本格局与变化,并对其全球价值链地理微观特征作了深入分析,是对已有研究尺度的拓展。更进一步,尽管已有研究对电子信息制造业全球价值链或全球生产网络的形成进行了理论阐释,如有学者才采用全球生产网络中的成本-能力比率、市场需要、金融约束和风险环境等要素来揭示苹果产品零部件全球生产网络的动力机制[30]。但是,本文主要尝试利用全球化对应地方响应、市场化对应技术管制的这种相互对应的思想去阐释苹果产品零部件全球价值链的形成与变化,相比已有研究可能具有更强的解释力,同时也是构建新解释框架的一种尝试,未来还需进行更加深入的分析与检验。

致谢

真诚感谢匿名评审专家在论文评审中所付出的时间和精力,评审专家对本文研究思路、价值链等级划分、图表展示与结论梳理等方面的修改意见,使本文获益匪浅。感谢朱晟君研究员、徐伟教授对本文初稿提出的宝贵建议。

参考文献

Introduction: globalisation, value chains and development

Making connections: Global production networks, standards, and embeddedness in the mobile telecommunications industry

跨国公司的组织模式与区位选择

The organization models and locational selection of multinational corporations

Multi-level modularity vs. hierarchy: Global production networks in Singapore's electronics industry

China's evolving role in Apple's global value chain

The semiconductor industry in South-East Asia: Organization, location and the international division of labour

The global assembly-operations of US semiconductor firms: A geographical analysis

The paper begins with a brief description of assembly processes in the semiconductor industry. The organizational structure and geography of the assembly operations of US semiconductor firms are then considered. Two issues in particular are examined, namely (a) the conditions under which vertical integration and disintegration of assembly tend to occur, and (b) the reasons why most semiconductor assembly is performed offshore. Lengthy empirical descriptions are offered of the assembly activities of US semiconductor firms in (a) the United States, (b) Western Europe, and (c) the world periphery and semiperiphery (above all, East and Southeast Asia). The paper concludes with a short critical comment on the theory of the new international division of labor.

The electronics industry in Southern California: Growth and spatial development from 1945 to 1989

Toward a dynamic theory of global production networks

Strategic sourcing: To make or not to make

Component sourcing strategies of multinationals: An empirical study of European and Japanese multinationals

Global value chains in the electronics industry: Characteristics, crisis, and upgrading opportunities for firms from developing countries

Mobile phones:Who benefits in shifting global value chains?

Partners for the China circle?

The governance of global production networks and regional development: A case study of Taiwanese PC production networks

How the iPhone widens the United States trade deficit with the People's Republic of China

全球电子信息产业价值链及对我国的启示

The development of global electronic and information industrial value-chain and its revelation

计算机产业全球生产网络分析:兼论其在中国的发展

Global production networks of computer industry and its development in Mainland China

The development of globalization and advancement of production technology further lead to the transformation of social production organization. New international division of labor has penetrated into the inner layer of products, and the global value chain and the global production networks have been brought into multidisciplinary research. The new theories can better explain the new changes of production organization in modern world. Based on introducing the concepts and remarks of global production networks, this paper firstly discusses the general organization of global production networks of computer industry. Secondly, according to two indexes of value increment and profitability, the paper proposes two kinds of smiling curve and takes the GPN framework to explain it, including value analysis and its spatial competition, corporation organization and power distribution. Thirdly, the paper studies the smiling curve of Chinese computer industry, and holds discussions on value and its spatial competition, and then discusses embeddness of Chinese computer industry to global production networks.

苹果手机零部件全球价值链的价值分配与中国角色演变

DOI:10.18306/dlkxjz.2019.03.009

[本文引用: 4]

产品内分工已成为支配当代企业分工与产品生产的重要模式。研究智能手机生产网络价值分配格局,对辨析中国大陆企业在移动通讯产业价值链中所处地位与演进具有重要意义。论文利用2012—2017年苹果公司供应商数据,以其零部件价值含量与技术要求为测度标准,分析了苹果手机零部件全球价值链的分配特征以及中国大陆企业在其中的地位变化。发现:高价值环节的供应商主要以美国、日本、韩国为主,而中低价值环节则以中国台湾、日本和中国大陆供应商为主,且中国大陆与中国台湾在中间环节占据重要地位。处于价值链高端的供应商分支数量在中国大陆和美国缩减明显,日本、韩国较为稳定,中国台湾增加明显。在价值链的中低端环节,供应商分支趋向中国大陆集中。印度、巴西以及越南等地成为新的中低端价值环节转移承接地。近年来,中国大陆在苹果手机价值链的高端环节得到了提升,长三角、珠三角、京津冀、成渝、中原地区等地逐渐形成了苹果供应商分支的集聚区域,呈现出零部件生产的区域分工特征。长三角(上海-苏州为核心)与珠三角(深圳-东莞为核心),承接了价值链多个生产环节,是中国大陆嵌入苹果手机生产网络的主要阵地。成渝地区既承接了芯片类企业布局,也承接了价值链低端的组装代工和包装服务环节,呈现出在价值链两端双向承接的特征。环渤海、福建及湖南等地主要承接苹果手机价值链的中间环节,而中原地区主要以苹果手机组装与包装服务为主,承接价值链的低端环节。最后,论文从创新驱动、政府作用与外资等方面探讨了影响中国大陆地位提升的因素。

Value allocation and China's evolving role in the global value chains of iPhone parts

Based on the data of Apple suppliers from 2012 to 2017, this study conducted an empirical analysis of the global value chains of iPhone parts, and the changing role of Chinese enterprises according to the cost value of different parts of mobile phone. The conclusions are as follows: Firstly, suppliers of the key parts were mainly located in the United States, Japan, and South Korea, and they were in the core of value chain governance; while the important and general components were mainly from Japan and Chinese mainland and Taiwan, China. Secondly, the production of most parts was completed in Chinese mainland and Southeast Asia. In recent years, Chinese mainland's status of the "world factory" for general parts of iPhone has been further consolidated, but at the same time, breakthroughs have been made in some important links of the value chains, and Chinese mainland has gradually moved to the high end of the value chain. Thirdly, the Yangtze River Delta, the Pearl River Delta, the Beijing-Tianjin-Hebei region, the Chengdu-Chongqing region, and the Central Plains have become the core production base of iPhone's components. iPhone parts industrial clusters have been formed in the Yangtze River Delta and the Pearl River Delta, and they have become the main base for Chinese mainland's enterprises to embed in iPhone's global value chain. The Chengdu-Chongqing region is not only the base for chip companies, but also the location for assemblying and packaging services at the low end of the value chain, which indicates the two-way acceptance at both ends of the value chain. The regions around the Bohai Bay, Fujian Province, Hunan Province, and some other places mainly carry on the production of the medium part of the value chain, while the Central Plains mainly carry on the production of the mobile phone assembly and packaging services. Finally, we analyzed the driving factors that upgraded Chinese mainland's status in the global value chains.

全球价值生产的空间组织:以苹果手机供应链为例

DOI:10.11821/dlyj020190903

[本文引用: 4]

采用2012年与2019年苹果手机全球供应商数据,基于GPN 2.0的相关理论建立分析框架,探索苹果手机全球生产网络中主要行动者类型、行动者策略、进入与退出动态、地理分异性、网络动力机制和战略耦合机制。该网络主要行动者是美国、日本、韩国、中国大陆、中国台湾省,布局全球生产网络的热点地区在亚洲;网络中有六类行动者,行动者策略是企业间控制与企业间合作,网络产生和演化的动力机制为成本-能力比率、市场需要、金融约束和风险环境,主要行动者通过本土创新、国际合作关系和生产平台战略耦合机制嵌入苹果手机的全球生产网络。最后,从转型创新模式、孵化自主供应链角度对中国行动者产业升级提出对策建议。

Spatial organization of global value production: A case study of supply chain of Apple's iPhone

Globalization has been reshaping the way of local industries connecting with the global economy. With the rise of emerging economies and regional production networks in East Asia, the traditional division of labor in mobile phone manufacturing industry is changing. This paper uses the data of iPhone's global suppliers in 2012 and 2019, and establishes an analytical framework based on the relevant theories of GPN 2.0, and explores the geographic differentiation, the competitive dynamics strategy of network, strategic coupling, entry and exit dynamics and regional division and evolution in China of iPhone's global production network. The study found the following: (1) The main actors of the network are the United States, Japan, South Korea, Chinese mainland and China Taiwan province, and the hot spots in the global production network are located in Asia; (2) There are six types of actors in the global production network of iPhone, and their strategies of configuring the global production networks interfirm control and interfirm partnership; (3) The competitive dynamics strategy are cost-capability ratios, market development, financial discipline and managing risks, in addition, the main actors have embedded the global production network of the iPhone through three strategic coupling models (indigenous innovation, international partnership and production platforms), which are deeply embedded in differentiated national/regional industrial policies, corporate strategies, location advantages (proximity effects), industrial clusters, government-enterprise relations, and business institution (family group in home economies); (4) iPhone's supply chain in China is dominated by foreign-implanted supply chain. Furthermore, the core components supplied by China's actors are optical devices and display/touch modules, and their advantages are reflected in system integration, incremental innovation and production-related R&D capabilities. Finally, based on the impact of trade war between China and the United States on China's participation in global division of labor, this paper puts forward suggestions from the perspective of transforming innovation model and incubating independent and controllable supply chain: (1) Radical innovation is not the only way to achieve industrial upgrading, in other words, successful incremental innovation or integrated innovation is more suitable for China's small and medium-sized private enterprises in the mobile phone manufacturing; (2) China's actors should incubate independent and controllable supply chain system on the basis of resource integration at home and abroad to enhance the global competitiveness.

Who profits from innovation in global value chains? A study of the iPod and notebook PCs

Capturing value in global networks: Apple's iPad and iPhone

Global production networks, knowledge diffusion, and local capability formation

Explaining geographic shifts of chip making toward East Asia and market dynamics in semiconductor global production networks

基于全球价值链的全球化城市网络分析:以苹果手机供应商为例

DOI:10.11821/dlxb202104007

[本文引用: 2]

本文基于2019年苹果手机供应商数据,从全球价值链视角构建全球化城市网络,将具有全球化职能的专业城市与世界城市纳入同一分析框架,运用社会网络与社区发现方法,研究了研发型、生产型、代工服务型城市网络的节点中心性、整体拓扑结构、社群结构及影响机制。结果发现:① 苹果手机零部件的全球化城市网络均具有多中心与多样化、节点等级化、联系外部化特征,网络中“明星”节点高权力—高声望并存且权力总体高于声望;② 研发型城市网络联系最紧密,趋于首位城市分布,小团体结构与集群发育明显。生产型网络关联性最高,网络趋于均匀结构与位序—规模分布。代工服务型网络中心性最高,权力集中在少数城市节点,众多节点易受核心节点控制与支配。③ 研发型城市社区集群最明显,企业通过知识关联效应形成专业化集群,获取本地化经济益处,并通过链式与轮轴式布局建立基于关系接近的跨国网络社区。生产型城市社区集群次之,企业通过经济关联效应形成一般化集群,获取城市化经济益处,通过网络式布局建立基于地理接近的本国内跨行政区网络社区。代工服务型城市社区未发育出明显集群网络,企业通过低成本关联实现规模经济,世界工厂模式形成散点式网络社区。

An analysis of the multidimensional globalizing city networks based on global value chain: A case study of iPhone suppliers

Based on the data of 197 suppliers of iPhone components and parts in 2019, this paper builds multidimensional world city networks from the perspective of global value chains, integrating specialized cities with global functions and the high-class world cities into the same analytical framework, which enriches the research perspective of world city networks in the era of globalization to a certain extent. The purpose of this paper is to expand the research and investigation scope of the existing field of world city networks. By means of social network analysis (i.e. the analysis of centrality, connectedness and network cohesion), rank-size rule and community detection, we study the power and prestige, the overall topological structure, the community structure and influence mechanism of the city networks of R&D-oriented, production-oriented and OEM service-oriented types. The results show that: (1) All the world city networks are characterized by polycentricity and diversification, differentiation of nodes' status and dependence on external connections. The "star" nodes in the network coexist with high power and high prestige, and the power is generally higher than the prestige. (2) The network cohesion and rank of R&D-oriented cities are the highest, and the network tends to show a primate city distribution, and the growth of small group structure and the phenomenon of R&D clusters are obvious. The production-oriented network has the highest connectedness, and it tends to present a rank-size distribution and an equilibrium structure. Its network scale is large, but the ties of many nodes are sparse and decentralized; OEM service-oriented network has the highest relative centrality, and power and information are concentrated in a few city nodes. (3) The cluster characteristics of R&D-oriented city communities are most noticeable. Moreover, the network has significant long-distance knowledge spillover and cooperation behavior. Enterprises form specialized clusters in R&D-type cities through non-tradable interdependence, and obtain the benefits of localization economies and spatial integrated effects. The cluster tendency of production-oriented city communities are relatively obvious. Geographical proximity and spatial dependence are the main factors incubating community structure. Enterprises form generalized clusters through tradable interdependence to obtain the benefits of urbanization economies and distance attenuation effect. No obvious cluster network has been incubated in OEM serviced-oriented city communities. Polarization phenomenon of the inter-community is extremely significant, that is to say, the core city community in Taiwan, China, radiates to other low-level equilibrium communities, forming a radial community structure. Contract manufacturers seek the cities with low labor costs around the world to carry out standardized production, and realize full competition through scale economies, therefore, a scatter-type city network layout structure is formed.

Who captures value in a global innovation network? The case of Apple's iPod

The distribution of value in the mobile phone supply chain

Integration of four-phase QFD and TRIZ in product R&D: A notebook case study

经济全球化变革下的世界经济地理与中国角色

DOI:10.11821/dlxb202202004

[本文引用: 2]

经济全球化浪潮下的世界经济地理格局和中国角色演变一直以来都是学术界关注的热点问题,然而当前学界偏重从国家经济模式和国际贸易角度来解释这种格局的变化,而较为缺乏基于生产组织视角的经济地理解释。因此,本文从经济地理视角出发,解析经济全球化浪潮下世界经济地理格局变动与中国角色的演变。本文揭示了在三次全球化浪潮的冲击下,世界经济地理格局从“核心—边缘”到“链式重构”再到“网络不均衡”的演变过程,以及经济全球化的驱动力如何从“贸易全球化”转变为“生产全球化”,继而朝“多元全球化”演进。本文还论述了中国如何通过战略耦合模式的动态调整实现从经济全球化的参与者到变革者的转变。本文认为这种角色转变,改变了西方发达经济体对后发经济体的预设发展路径,以及经典的产业梯度转移理论所预测的空间秩序,为全球化格局的变动带来新的重构动力与可能。最后,本文结合此次新型冠状病毒肺炎疫情全球爆发带来的影响对未来经济全球化发展存在的可能路径进行分析,并从经济地理学视角为中国未来经济全球化发展道路选择提供了参考建议。

The dynamics of world economy geography and the role of China in economic globalization

From the perspective of economic geography, this paper studies the changing spatial pattern of world economy and China's role in different waves of economic globalization. Firstly, this study finds that the geographical pattern of world economy changes from "core-periphery" to "chain-reconfiguration", and to current "network-imbalance". Meanwhile the driving force of economic globalization shifts from "trade globalization" to "manufacturing globalization". At present, "multiple globalization" is involving into a new engine to driving the development of economic globalization. We then discuss that how China changes its role in economic globalization by changing modes of strategic coupling. We argue that the role transition of China breaks the traditional developing path which developed countries set for developing countries and theoretical spatial order put forward by classical industry gradient transfer, bringing new restructuring power and possibility for changing pattern of globalization. Finally, we discuss the impacts of COVID-19 pandemic on the development of economic globalization and the development trend of economic globalization in the post-pandemic era. Based on the analysis, we come up with some suggestions regarding to the potential development paths of China under the background of economic globalization.

网络型国际产业转移模式研究

Studies on modes of international network- like industry transfer

1978年改革开放以来中国工业地理格局演变

DOI:10.11821/dlxb201910002

[本文引用: 2]

回顾改革开放40年,在深刻的制度变革环境下,中国工业实现快速发展,中国工业地理格局也在经济转型中得到重塑。中国工业总体上经历了从内陆扩散到沿海地区集聚,再向内陆转移的过程。但不同类型产业地理格局及变化受制于不同力量,显现出一定的行业差异性。与改革开放之初相比,中国工业在不同地理尺度上呈现出明显的集聚趋势,但集聚程度较欧盟和美国低。产业的聚集与分散驱动不同尺度下的产业迁移,导致区域产业频繁进入和退出,促使地方产业呈现多样化态势,推动中国工业地理格局演变。从经济转型的视角出发,改革开放可概括为市场化、全球化和分权化三个过程,这些过程创造市场力量,激活地方力量,引入全球力量,共同重塑了中国工业地理格局。

Evolution of Chinese industrial geography since reform and opening-up

Looking back on the 40 years of reform and opening-up, Chinese industry has achieved rapid growth and development, and Chinese industrial geography has been profoundly reshaped under the profound institutional evolution environment. Chinese industry has undergone a process of spreading in the inland to agglomeration in the coastal areas and then dispersion towards the inland again. However, the geographical pattern of different types of industries is influenced by different forces, leading to differences in the spatial restructuring process. Since the beginning of reform and opening-up in 1978, Chinese industries have been increasingly more agglomerated at different geographical scales, but still much lower than the European Union and the United States. Industrial agglomeration and decentralization drive industrial migration at different scales. In spite of the heterogeneity of industries, industrial migration has generally changed from a scattered layout to an agglomeration pattern in coastal areas; and in recent years, industrial migration has gradually shifted from developed eastern provinces to central provinces, indicating a new round of industrial migration. Remarkable regional industrial entries and exits have promoted the evolution and diversification of local industries. Overall, Chinese industrial space tends to be more complex and concentrated, the links between industries are further strengthened with a more obvious "path dependence" characteristics of industrial evolution in coastal areas. Theoretically, Chinese economic reform is not only the reform of development mode, but also the reform of institutions in essence. The fundamental triple process of marketization, globalization and decentralization has introduced market forces, local forces, and global forces to reshape Chinese industrial geography. And for the study of Chinese industrial geography, besides continuing to summarize patterns and dynamics from multiple perspectives, it is necessary to reveal the deep-level mechanism of the evolution of industrial geography pattern through phenomena, and evaluate the multiple effects of the reshaping of industrial geographical pattern systematically.

中国经济地理学的发展方向

The development directions of China's economic geography

北京市外资制造企业的区位分析

Locational study of foreign enterprises in Beijing based on an ordered probit model

Foreign direct investment has been a key driving force for China's urban development since the economic reform and opening up. Beijing is one of the favored locations by foreign investors. Foreign enterprises in Beijing have played a significant role in restructuring its production spaces and industrial compositions. Compared with their domestic counterparts, foreign enterprises are rational decision-makers and have more flexibility and freedom in choosing their locations. Governed by market forces, foreign enterprises are not randomly distributed within a city and their locational patterns are detectable. Based on data from the second census of basic units, this paper attempts to picture the spatial patterns of foreign enterprises in Beijing. Efforts are further made to investigate the locational behavior of foreign enterprises by incorporating firm-specific, industry-specific and location-specific factors in an ordered probit model (OPM). Empirical results show that foreign enterprises in manufacturing tend to agglomerate in the central city, but being diffused to the remote suburbs and having indeed promoted the industrial suburbanization in Beijing. Statistical results suggest that large and newly established manufacturing enterprises favor the suburbs while wholly foreign owned manufacturing enterprises and those producing multiple types of products tend to locate in the inner city. Industrial agglomeration pushes foreign manufacturers to the suburbs. Industry-specific factors play a crucial role in determining locations of foreign enterprises in Beijing. Those in resource and labor intensive sectors are inclined to locate in the suburbs while those in capital and technology intensive sectors are likely to favor the central city. The results have important policy implications for urban industrial restructuring in Beijing.

外商直接投资对上海经济发展影响的分析

An approach to FDI’s impact on economic development of Shanghai

全球电子信息产业贸易网络演化特征研究

The geography of global electric information industry trade network

企业地理集聚与区位选择

DOI:10.13284/j.cnki.rddl.002997

[本文引用: 1]

企业区位是理解区域经济转型与空间重构的微观基础。本课程全面回顾了区位研究的理论视角及其发展,归纳总结了企业地理集聚的影响因素、基本假设以及相关的经济地理学议题。最后,从珠三角外资制造业企业地理集聚中寻找微观证据,运用地理空间分析方法与空间模型,探索企业异质性对于FDI区位的现实影响。主要观点如下:

Firm's geographical agglomeration and location choice

<p>Firm’s Geographical Agglomeration and Location Choice</p>

模块化视角下大陆台资电子信息产业价值链的时空演变

The temporal and spatial evolution of the value chain of Taiwan-funded electronic information industry in Mainland from the modular perspective

全球价值链模式的产业转移:动力、影响与对中国产业升级和区域协调发展的启示

Industry transference of GVC mode: Force, influence and inspiration for China's industrial upgrading and balance development of area

中国城市价值链功能分工及其影响因素

DOI:10.11821/dlyj020191045

[本文引用: 1]

价值链的空间重组正在深刻的改变着城市体系的经济景观,建立在价值链分工基础上的城市功能结构的研究已经成为经济地理学的重要课题。将中国上市公司500强企业网络划分为公司总部、商务服务、研究开发、传统制造、现代制造、物流仓储和批发零售七种类型功能区块,研究了中国城市价值链功能分工及其影响因素。结果发现:沿着价值链的功能分工已经成为中国城市体系经济景观的显著特征,功能多样化城市和功能专业化城市并存于中国城市体系,东部地区和城市密集地区的城市在价值链分工中占据了更好的地位;中国城市按照价值链中的优势功能可以划分为九种类型,少数城市转变为承载公司总部、研究开发、商务服务等多样化功能的高等级中心城市,而大量中小城市则转变为传统制造专业化基地;市场潜力、关键资源、区位条件、营商环境等城市属性特征是城市功能分工的重要影响因素,城市资源、区位可达性等属性特征的增强将提高城市成为总部基地、商务中心和研究基地的概率,而降低城市成为传统制造基地的概率。

Patterns and determinants of functional division of cities across product value chain in China

Decreasing spatial transaction and trade costs facilitates the geographical fragmentation of functions, i.e. the stages or activities within product value chain could give rise to functional differentiation of cities. Despite the recent advances in the study of the spatial structure of urban networks, the analysis of functional differentiation of cities across multi-location firms' value chain has been largely neglected. The study sets out to investigate the patterns of functional division of economic activities within China's urban system, and explore the underlying factors with multiple regression models. To this end, data on the corporate networks of China's top 500 public companies in 2018 are collected, and the establishments within the corporate networks are grouped into seven functions: headquarters, business services, research and development, modern manufacturing, standardized production, logistics, and wholesale and retail. The following results are obtained. First, different types of functions within the value chain show different spatial patterns, which leads to the differentiation of urban functions, and promotes the transformation of Chinese cities from sectoral specialization to functional specialization. The three knowledge-rich functions of headquarters, business services and research and development are mainly centralized in the core cities of China's major urban agglomerations, while standardized production has the lowest level of spatial concentration. The second major finding is that functional specialization co-exists with functional diversification within the urban system in China. Overall, large cities are much more functionally diversified, while small and medium-sized cities tend to be specialized in standardized production. Using the clustering algorithm based on self-organizing feature maps, the 334 cities in China can be classified into 9 functional types. Third, location fundamentals play a key role in driving the functional differentiation of cities. Although city size, vital resources, accessibility, urban infrastructure, business environment positively contribute to the presence of all functions, their marginal effects differ across the seven functions. The improvement of economic scale and vital resources will increase the probabilities for cities to develop into headquarter centers, business service centers and R&D centers, while reducing the probabilities of cities is becoming standardized production bases. The traditional urban resource advantages has been transformed into the competitive advantages of urban functional status, suggesting that the development gaps between cities in China will further be enlarged under the network environment.

北京电子信息产业及其价值链空间分布特征研究

The spatial distribution of electronic information industries and its value chain parts in Beijing

As a leading sector, electronic information industries in Beijing have strong strength and good prospects.The present studies focus on the analysis of the spatial distribution of high technology industries and electronic information industries.There have been relatively few studies on the spatial distribution of electronic information industries from the perspective of enterprises, especially on the spatial distribution of main value chain parts.</br>This paper selected 30 large electronic information enterprises to do study based on the research on spatial distribution of electronic information industries.We collected its information about spatial distribution in Beijing by reading 2011 Report of Transnational Corporations in China, browsing official websites and so on.This article analyzed the spatial distribution of headquarters, research departments, production departments, sales and marketing departments in Beijing.The conclusions are as follows.The electronic information industries were obviously suburbanized and agglomerated in suburban areas.The main value chain parts of large electronic information enterprises were also agglomerated and the suburbanization of production departments most obvious.The spatial distribution of electronic information industries and enterprises exhibited a polycentric spatial structure. The functional division among main electronic information industries agglomeration areas and the regional division based on value chain of large electronic information enterprises had emerged.

中国产业发展与布局的关联法则

DOI:10.11821/dlxb202012010

[本文引用: 1]

产业地理学研究产业空间分布及其动态演化规律。基于地理邻近性的集聚理论揭示了产业地理不平衡分布的内在机制。演化经济地理学借鉴演化经济学的历史视角,从历史角度考察经济活动空间分布的渐进演化机制,认为地理邻近性不是产业地理格局演化的充分必要条件,以认知邻近性为核心的多维邻近性能够提供更好的解释。本文从认知邻近视角系统地分析了中国区域产业发展与布局动态演化规律,总结出中国产业发展与布局的“关联法则”,即一个企业或区域进入(或退出)某项经济活动的概率是该企业或地区拥有的基于相关知识基础的经济活动的函数。本文全面地回顾了关联法则涉及的关键概念,梳理企业和区域尺度的实证研究成果,讨论关联法则在中国的适用性及其补充和拓展。本文指出:① 在认知邻近视角下,基于资源转换和组织学习等理论基础,关联法则研究了企业或区域发展新产业与现有产业之间的关系。② 关联法则不仅适用于中国企业和区域尺度,还会影响区域经济发展、创新和韧性等。③ 外部联系、冲击以及内部制度环境等可能会降低区域产业动态对本地产业基础的依赖性。关联法则指出中国区域需培育内生发展模式,围绕现有区域能力、技术和知识积累发展区域产业和实现区际产业优化布局与分工,逐步建立相关多样化的产业体系,增强区域韧性,支撑国内经济循环。

The principle of relatedness in China's regional industrial development

Geographical distribution and agglomeration of industries have been a long lasting concern of economic geographers. Some studies have stressed geographical proximity and industrial agglomeration as the key driving force of uneven distribution of industries. Recently, evolutionary economic geography, based on evolutionary economics, has adopted a dynamic and historic perspective to study the evolution of regional industrial dynamics. It argues that geographical proximity is neither sufficient nor necessary for efficient knowledge spillovers; instead, it calls for more attention to the idea of cognitive proximity as well as its importance in regional industrial dynamics. The idea is that for knowledge spillovers to take place effectively, some kind of cognitive proximity in terms of shared competencies must be in place. Inspired by this, we examine China's regional industrial development through the lens of cognitive proximity, and propose the "principle of relatedness", that is, the probability of a region to enter/exit one specific economic activity is heavily dependent on regional pre-existing economic profile and local knowledge base. This paper first introduces some key, relevant concepts, and then reviews empirical studies that are underpinned by the "principle of relatedness". Furthermore, it discusses the applicability of "principle of relatedness" in the Chinese context. Our main findings are as follows: (1) theories on resource base view and knowledge spillovers both support the existence of the "principle of relatedness"; (2) the "principle of relatedness" enables us to better understand China's regional economic development, innovation and resilience; however, (3) the effectiveness of the "principle of relatedness" may be compromised by external shocks and internal institutions. One policy implication from the "principle of relatedness" as well as our empirical research is that Chinese regions should seek to diversify related industries and enhance related variety of their regional profiles. In doing so, they are able to become more economically resilient and achieve more sustainable economic development.

关于产业区位问题的解读

On the interpretation of industrial location problem

全球生产网络、航空网络与地方复合镶嵌的战略耦合机理

The strategic coupling of global production network, aviation network and local development

Market rebalancing of global production networks in the Post-Washington consensus globalizing era: Transformation of export-oriented development in China

维达力,在赤壁发力

Vidali, in Chibi power

中国苹果零部件供应链空间组织研究

Spatial organization and influencing factors of Apple's component supply chain in China

Globalisation in reverse? reconfiguring the geographies of value chains and production networks

Standing at a crossroads, where ongoing ‘slowbalisation’ coincides with new forces such as the outbreak of the Covid-19 pandemic, heightened geopolitical tensions, the emergence of disruptive technologies and the increasing urgency of addressing environmental challenges, many important questions remain unsolved regarding the nature and impact of the current economic globalisation. This special issue on ‘Globalisation in Reverse? Reconfiguring the Geographies of Value Chains and Production Networks’ aims at showcasing recent work that seeks to contribute to, and advance, the debates on economic globalisation and the reconfiguration of global value chains and production networks. This introductory article has three objectives: first, based on a broad literature review, we aim to identify four key forces, as well as the fundamental relatively stable capitalist logics contributing to the complex reconfiguration of global economic activities. Second, we will position the papers included in this special issue against the four main forces identified and discuss the contributions of each article to capture some emerging cross-paper patterns among them. Finally, we outline the contours of a research agenda that suggests promising avenues for further investigation of the phenomenon of value chain and production network reconfigurations in times of uncertainty.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}